By Jon Schweppe, Senior Advisor, American Principles Project

Hey there.

As many of you know, I’m back at American Principles Project (APP) after a year-long stint serving in the Trump Administration. My time working at the Federal Trade Commission for Chairman Andrew Ferguson was incredible — and I’ll write more about that soon.

But I wanted to tell you about my new gig at APP. I’ll be heading up a new policy initiative to build out an “Affordability Agenda” that we hope the Republican Party will adopt in 2028 and beyond.

While social issues remain an integral part of the Republican Party’s messaging strategy — and are certainly key to maintaining a majority governing coalition — it’s become very apparent that connecting with our voters on economic issues is going to be an important part of winning going forward.

How do we do that? Well, for starters, we provide them with Populist Solutions to address their biggest affordability concerns: wages, food, education, energy, healthcare, and housing.

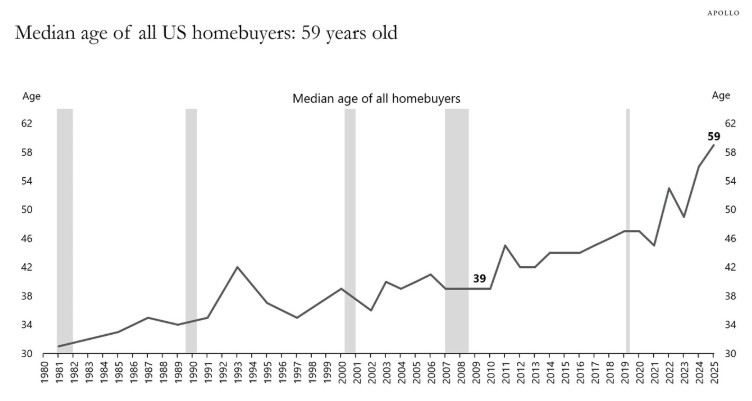

So, let’s start with that last one. Young people have been completely priced out of homebuying.

And it’s getting worse, not better.

According to a recent survey from the National Association of Realtors, the median homebuyer was a 59-year-old. That’s older than the Big Mac.

Access to homeownership is a core part of achieving the American dream. Take it away, and leftist vultures like Zohran Mamdani, who rode the dissatisfaction of young people to the New York City mayor’s office, will take advantage and benefit politically. This is how democracy fundamentally works: if the “reasonable party” ignores a problem that voters care about for long enough, the people will often decide to vote for the lunatic with the magic beans.

Obviously, Republicans gotta do something. Even if it gives some Senate Republicans heartburn.

Home Savings Accounts (HomeSAs)

Here’s an idea that Terry Schilling described in his thread above: what if we provided potential homeowners with a significant tax incentive to save their hard-earned money for a few years in order to finally purchase a new home?

It’s not like this is a novel approach. The “HomeSA” idea borrows directly from the framework of Health Savings Accounts (HSAs), enacted in 2003, which have demonstrated the efficacy of incentivizing individual savings.

HSAs have been one of the few healthcare policy success stories:

Taxpayers Win Big: According to the Kaiser Family Foundation, taxpayers are expected to save $180.9 billion from HSA tax deductions over a 10-year period from 2025 to 2034.

Widespread Adoption: By the end of 2024, more than 39 million HSAs existed, serving approximately 59 million individuals.

Powerful Savings Vehicle: HSA assets totaled nearly $147 billion at year-end 2024. Accounts with investments averaged more than $22,000, demonstrating HSAs’ role as a potent vehicle for wealth accumulation.

We can apply this same bottom-up, dynamic approach to the housing market, allowing young people to afford homes without taking a sledgehammer to the housing market. Instead, let’s focus on the demand side and give people the opportunity to save, invest, and finally afford.

APP’s proposal would allow for individuals to contribute up to $5,000 pretax to their HomeSA account each year. (Married couples would be eligible to contribute up to $10,000 pretax.) They could then invest those contributions to make their savings work harder, potentially turning annual contributions into a large nest egg fairly quickly.

Like with HSA accounts, HomeSA dollars would be limited for a specific purpose. Withdrawals would only be tax-free if the funds went toward either a down payment, or toward excess mortgage principal payments, on a primary home.

I particularly like the idea of encouraging homeowners to pay down their home faster, saving them tens of thousands (and often hundreds of thousands of dollars) over the life of their mortgage. For the first time in the post-ZIRP era, homeowners would avoid the perverse incentive of embracing mortgage debt.

Importantly, this proposal aligns perfectly with President Trump’s housing agenda. He’s already taken decisive action by directing Fannie Mae and Freddie Mac to purchase $200 billion in mortgage-backed securities to ease borrowing costs and lower mortgage rates.

But the President knows true affordability isn’t about artificially crashing prices and wiping out homeowners’ hard-earned wealth. As he explained in a January 29th Cabinet meeting: “I don’t want to drive housing prices down. I want to drive housing prices up for people that own their homes, and they can be assured that’s what’s going to happen.”

HomeSAs honor that principle by boosting demand-side tools, via cheaper financing through personal savings, all while protecting existing owners’ equity. Rather than flood the market with risky supply that benefits speculators, HomeSAs would empower families to invest in their future.

Originally published on Populist Solutions.